On Ethereum's issuance policy, inflationary, deflationary or equilibrium?

(Special thanks to Anders Elowsson and Justin Drake from EF for discussion on this topic)

Since Ethereum moved to PoS last September, the issuance rate of ETH has reduced dramatically compared to that of the PoW era. The topic of ETH being Ultra Sound Money is getting widely discussed by the Ethereum community, as illustrated by the work by the ultrasound.money team. The Ultra Sound Money idea mainly centres around three key areas:

The reduced issuance of ETH, whether ETH will be deflationary and eventually reach an equilibrium?

Ethereum as the most secure, anti-fragile, decentralised and efficient smart contract blockchain, allowing it to secure the internet of value.

The scarcity, security and utility of Ethererum, leading to ETH’s use as a store of value (SoV) and economic collateral, forming a monetary premium that is beyond its basic utility, which further enhances Ethereum’s security and utility - a flywheel effect.

In this post I will focus on the first point: try to reason about the inflation/deflation dynamics of ETH. And ask the question: what are the forces that drive this dynamic? Will there be an equilibrium state where ETH’s issuance is 100% offset by the burn?

If the reader doesn’t want to read the whole post, below is the TLDR:

ETH deflation is driven by blockspace supply-demand - intrinsic utility.

ETH inflation is driven by staking yield demanded by stakers - which reflects their perceived prospect of ETH as a long term SoV.

The deflationary and inflationary forces have two separate distinct supply-demand markets that tend to balance out each other. However, it is unclear that an equilibrium of the total ETH supply will form with the current issuance design. A more likely scenario is that ETH will be alternating between periods of (low)deflation and (low)inflation, depending on factors such as blockspace supply growth (L2) and demand, market cycle (both crypto and traditional market), competition for SoV assets etc.

In practice, Ethereum will probably stay deflationary in the medium term (2 to 5 years is my estimate) until the aforementioned stable period begins. The current deflationary nature can be viewed as ETH the asset being undervalued, relative to the intrinsic value accrue.

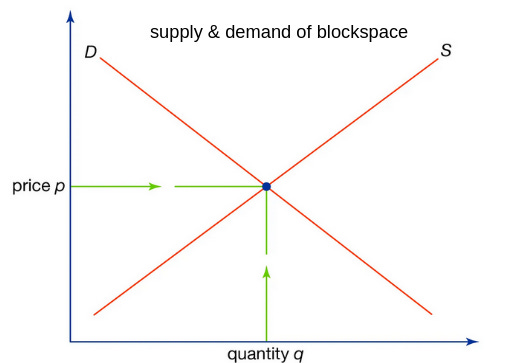

Supply and Demand of Blockspace

The intrinsic utility of ETH is to pay for transaction inclusion within blockspaces on Ethereum. In trying to answer the question of whether ETH is inflationary, or deflationary, we first need to look at the supply and demand of Ethereum blockspaces:

Price: The price of blockspace is denominated in ETH. At different price levels, the S line represents the amount of blockspace supplied, the D line represents the amount of blockspace demanded.

Demand: From a high level, the demand for blockspace includes use cases such as NFTs, token trading, DAO coordination, identity services, token transfers etc, and over the medium to long term, settlements of L2 transactions.

Supply: The supply of Ethereum blockspace at different price levels (transaction gas price) is not perfectly elastic. Throughout Ethereum’s history, the block gas limit has been gradually increased: from 5000 gas limit in July 2015 to 30 million in Jan 2023 (the current 30m limit is the max size, with 15m being the target average gas limit).

The chart below shows the increase of gas limit over time (RHS), along with average gas price in gwei (LHS). Several notable historical events were highlighted to explain the spike in blockspace demand (ICO, CryptoKitties, Defi Summer, MEV etc)

Looking at the above chart, it is clear that whenever supply increases (the blue line), the demand catches up (the green line). It can also be interpreted the other way around: the supply of blockspace has been increasing in response to the ever increasing demand.

The room for significant further increase of blockspace on Ethereum L1 is limited given Ethereum’s fundamental requirement of maximum decentralisation, which in turn results in limitation on block-proposer machine spec, storage bloat, block time, network traffic etc.

Whilst L1 blockspace supply is limited, the rapid development of L2s (optimistic, ZK rollups, validiums etc) will serve to fill the gap for further demand, while offering different security guarantees and different maturity.

It is difficult to predict the future supply demand dynamics of Ethereum blockspace. With Ethereum being the most secure smart contract L1 blockchain, we can make a case that the demand for high-security, high-value will remain on L1, while lower-value ones gradually migrate to L2s.

Deflationary force: intrinsic utility leads to ETH Burn

Compared to fiat currencies, gold, or many other cryptocurrencies, one key difference of ETH is the burn mechanism (aka, EIP-1559). Since the activation of EIP-1559 on Aug 5 2021, base fees paid for transaction inclusion on Ethereum are burned. Given the same blockspace supply, higher demand leads to higher base fee, which results in greater amount of ETH being burnt (see Figure 1 above for example).

During the bear market in January 2023, the network averaged 18.3 gwei base fee (screenshot below from ultrasound.money). At this rate roughly 720,386 ETH will be burnt per year.

For this analysis, I will consider the following demand scenarios. They merely serve as examples that can help the readers make their own judgement.

Moderate demand of blockspace: in this scenario, blockspace demand out-grows supply, we can use a conservative estimate of 25 gwei, roughly 50% of the historical average of 52 gwei base fee since EIP-1559.

Low demand for blockspace, we can use a gas base fee of 15 gwei, this is based on the lowest historical quarterly average base fee since EIP1559, observed in Q3 2022.

Current demand as of Jan 2023 as a comparison, at 18 gwei.

New Issuance

Post Merge in Sep 2022, Ethereum transitioned from Proof-of-Work (POW) to Proof-of-Stake (POS). Under the POS consensus mechanism, newly issued ETH is awarded to stakers who stake their ETH to secure the Ethereum network. This is the only source of new issuance.

The issuance mechanism is based on the following formula, as per Vitalik’s annotated spec:

Issuance = Gwei(effective_balance * BASE_REWARD_FACTOR // integer_squareroot(total_balance) // BASE_REWARDS_PER_EPOCH)

BASE_REWARD_FACTOR is a constant value of 64 hardcoded in the protocol.

There are 82181.25 EPOCHs per year.

Define D as total_balance (total staked ETH balance)

We then have Yearly Issuance I:

Define the constant 2.6 = c then we have :

We can calculate the staking yield y for stakers as:

The key point to highlight is that the issuance amount I, and staking yield y are both a function of the staked ETH balance (rather than the staking ratio). The higher the staked balance, the higher the issuance and lower the staking yield.

With a staked balance of 16M ETH as of Jan 2023, Ethereum issues 665,600 ETH per year.

Inflationary force: the supply and demand of staking yield - SoV.

The supply and demand of staking yield is a different market from the supply and demand of blockspace.

The staking yield demanded can be viewed as a risk-adjusted return of ETH the asset, which can be decomposed into:

Premium relative to some risk-free rates, such as US Treasury Bills.

Premium as a store of value, which can be relative compared to other SoV, such as gold, bitcoin, or fine art etc.

Opportunity cost compared to the potential economic return offered by spot ETH utility.

Items 1 and 2 are largely dependent on the social consensus regarding ETH the asset as a long term SoV. The more demand for ETH as SoV, the more demand for staking. (As a thought exercise, imagine passive investors who hold ETH as a long term SoV investment, why wouldn’t they staking it to earn yield instead of holding spot ETH?)

Item 3 can be viewed in the same vein as traditional Money Market, where the money demanded reacts to the interest rate.

In Keynesian economics, typically there are three motives for money demand, which are self-explanatory:

Transaction demand

Precautionary demand

Speculative demand

Putting the above framework within the Ethereum economy: ETH token holders need to make a choice: to balance their holding of ETH as utility money (to spend/invest within the crypto-economy), vs staking ETH as a long term SoV (LSD offers a middle house, which is a separate topic).

Plotting the relationship among the forces that drive inflation/deflation.

Given the above analysis of ETH’s intrinsic utility that drives deflation, and staking yield demand that drives inflation, we can plot them in Figure 3 below:

The LHS axis shows the amount of ETHs issued (dark blue line) or burned per year. The yellow, purple and red dotted line illustrate the amount of ETH burnt per year based on the low, moderate and current blockspace-demand scenarios, at 15, 25 and 18 gwei base fee. The green solid line shows the staking yield (RHS axis), and the light blue line shows the net inflation (issuance minus burn, over total supply).

Ethereum is currently deflationary.

We can observe that, currently Ethereum is slightly deflationary (-0.04%), with a staking yield around 4.16% (note MEV yield is not included).

The network cannot stay deflationary perpetually, i.e. total ETH supply cannot go to zero, so at some point one or both of the following dynamics will happen:

Burn may decrease (reduce deflation).

and/or Issuance may increase (increase inflation).

What might cause the above dynamic to develop?

In the deflationary regime, will ETH burn decrease?

In order to transact on Ethereum, burnt ETH will need to be repurchased. In theory, given the same blockspace demand, a deflationary ETH supply will overtime drive its fiat price to increase, which should reduce the blockspace demand - too expensive to transact? (condition 1 above).

From a data point of view, the above argument is inconclusive. As the chart below tries to investigate, does increasing ETH price reduce gas price? The green and amber lines show historical daily transaction count, and ETH price, log scaled to percentage value since genesis, while the red line shows gas price in gwei. Looking at the data, we firstly note that transaction count per day has plateaued around the network limit. It is however hard to conclude that raising ETH price will directly lead to lower demand (low gas fee), as we can see in each bull market (blue arrow), the increasing ETH price has been associated with increasing gas price. What we may infer from the data and above theory, is the increasing ETH price should create a dampening effect on demand, or has a legged effect on reducing demand.

Will issuance increase to reach an equilibrium with burn

The yield that stakers receive consists of two components:

the POS staking yield.

MEV yield.

As discussed earlier, the main driver for stakers to stake ETH, is the prospect of ETH the asset as a long term SoV, which may be reinforced during a deflationary period, as well as during a bull market (and vice versa). The increased issuance from staking will therefore somewhat offset the burn from utility. However it is difficult to mathematically prove that the issuance will increase to 100% offset the burn.

A more likely scenario is that ETH will be alternating between periods of (low)deflation and (low)inflation.

Conclusion and prediction:

Let’s finish with some examples to show Ethereum’s net inflation in different scenarios and make some practical predictions:

There is on-going research on the max number of validators in the long term, one proposal is 2^25 at 33.5m. At an average staking deposit rate of 20k ETH per day, it will take almost 3 years to reach the 33.5m deposit limit. We can safely assume that the staking amount will reach this limit, given the SoV appear of ETH the asset, plus the prevalence of LSD meaning even staked ETH can still indirectly participate in the crypto-economy.

As shown in the table above, even at moderate gas base fee of 25 gwei, the network is still deflationary. So if you believe the network average gas fee will be above 25 gwei (remember this is half the average since 1559) , then Ethereum will be deflationary within the next 3 to 5 years. Afterwards a new period will begin where Ethereum will be alternating between periods of (low)deflation or (low)inflation, depending on factors such as blockspace supply growth (L2) and demand, market cycle (both crypto and traditional market), competition for SoV assets etc.

The current deflationary nature can be viewed as ETH the asset being undervalued, relative to the intrinsic value accrue.

The issuance formula

As a side note, the above analysis assumes parameter BASE_REWARD_FACTOR stays as a constant value of 64, and the issuance formula itself remains static. However it is possible that in the future if the Ethereum community wishes to, the issuance formula can be adjusted to offer finer control of Ethereum’s monetary policy which will change the dynamics discussed.